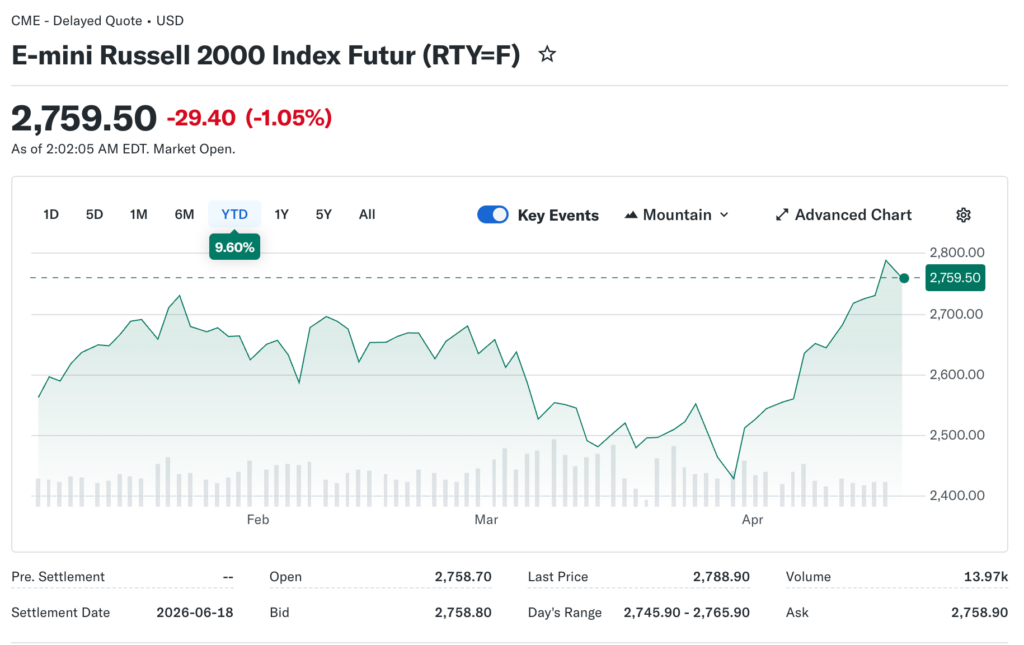

The Russell 2000 index surged past its previous all-time high on Friday morning during the trading session. The small-cap benchmark traded above 2,750, eclipsing the January peak of 2,735 points decisively. The breakout demonstrated broadening market participation beyond mega-cap technology leaders.

Lead financial expert Ryan Evans from Taurus Partners explores how small companies outperformed during recovery from the March lows. The index bounced approximately 14% from the trough, establishing impressive gains. This exceeded the S&P 500 rebound over the same period, showing relative strength.

The Leadership Rotation

Small-capitalization stocks typically lead during early recovery phases from market corrections. The risk-on sentiment favored higher-beta names with cyclical exposure to economic growth. Investors rotated capital from defensive mega-caps into more growth-oriented smaller companies aggressively.

The outperformance suggested genuine optimism about economic growth prospects materializing ahead. Small companies proved more sensitive to domestic economic conditions than multinationals. Their strength validated the recovery narrative beyond just mega-cap technology earnings.

The Valuation Opportunity

Small-cap valuations compressed significantly during the crisis, creating attractive entry points for buyers. Price-to-earnings multiples fell below historical averages, providing a margin of safety. The valuation reset attracted value-oriented investors seeking bargains.

However, earnings quality among small caps remained questionable across many index constituents. Many companies lacked profitability despite generating revenue growth. The dispersion within the index created substantial stock selection challenges.

The Economic Sensitivity

Small businesses faced greater challenges accessing capital during periods of financial stress. Credit availability improved markedly as financial conditions normalized following the ceasefire. The easier financing environment supported growth initiatives and expansion plans.

Consumer spending resilience particularly benefited domestically-focused small companies across sectors. Unlike large multinationals, small caps derived revenues primarily from the United States. The geographic concentration amplified exposure to domestic economic growth.

The M&A Catalyst

Acquisition activity picked up substantially as strategic buyers pursued attractive targets. Small companies offered bolt-on opportunities for larger competitors seeking capabilities. Private equity firms resumed dealmaking after pausing during the crisis period.

Takeover premiums provided a meaningful upside catalyst for small-cap investors. The M&A activity supported valuations across the entire index. Strategic value often exceeded standalone trading multiples significantly.

The Quality Dispersion

Wide performance dispersion existed within the small-cap universe, creating winners and losers. Highest-quality companies with strong fundamentals outperformed peers significantly. Weaker credits struggled despite the broad index strength lifting all boats.

Active management added substantial value in the small-cap space compared to passive. Stock selection mattered more than for large-cap indices with concentrated leadership. The market inefficiency created opportunities for skilled fundamental managers.

The Liquidity Concerns

Trading volumes remained relatively light for many small-cap names. The illiquidity created execution challenges for institutional investors managing large positions. Bid-ask spreads are wider than those of large-cap equivalents, increasing transaction costs.

Institutional investors faced capacity constraints when deploying capital in small-cap strategies. Position sizes necessarily limited by available daily liquidity. The structural issues prevented massive institutional capital flows.

The Sector Composition

Financials and industrials comprised significant weightings within the Russell 2000 index. Regional banks benefited from normalized credit conditions and net interest margins. Manufacturing companies gained from economic optimism about production activity.

Technology represented a smaller portion of the index versus the large-cap indices. However, software and IT services companies performed exceptionally well. The sector diversification provided a different exposure profile than the mega-cap benchmarks.

The Leverage Factor

Small companies typically carry higher debt loads relative to enterprise value. The leverage amplified returns during upswings, benefiting equity holders. However, downside risks are equally magnified during stress periods.

Interest coverage ratios varied widely across index constituents. Companies with strong cash generation managed debt comfortably. Weaker operators faced refinancing challenges at elevated rates.

The Growth Prospects

Revenue growth rates for small caps exceeded those of their large-cap counterparts. Smaller market shares allowed for easier expansion opportunities. The runway for growth justified premium valuation multiples.

Market penetration strategies delivered results as companies scaled operations. Geographic expansion within the United States provided an addressable market. The growth potential attracted investment despite execution risks.

The Earnings Leverage

Operating leverage materialized as revenues increased across fixed cost bases. Incremental margins exceeded company averages significantly. The earnings acceleration justified the premium valuations assigned.

However, execution risks remained elevated for smaller companies. Management quality and capital allocation discipline varied widely. Thorough due diligence essential for individual stock selection.

The Historical Patterns

Previous small-cap breakouts often preceded sustained multi-year advances. The leadership rotation from large to small caps historically positive signal. However, false breakouts also occurred, requiring confirmation.

Sustained trading above resistance levels is necessary for validating a breakout. Volume expansion would provide evidence supporting the breakout thesis. Technical follow-through is critical over the coming sessions and weeks.

The Investment Approach

Diversified small-cap exposure through low-cost index funds represented a prudent approach. Individual stock selection required substantial research capabilities and resources. The wide dispersion made passive indexing a reasonable strategy.

Active managers with proven long-term track records deserved consideration. Demonstrable skill-based alpha opportunities existed in this inefficient market. However, higher management fees needed a clear justification through sustained performance.